The Crypto-Carry Trade

This is not a crypto bull or bear case piece. It’s simply a discussion of some crypto-currency policy problems which must be addressed over the next few years. The way the US monetary system reacts to these problems or fails to will have huge consequences. The author is ex-faculty at a hedge fund and does math for a living, all opinions are his own, but facts are cited.

Definitions

- In a modern reserve bank economy the ‘interest rate’ is a rate of return on assets which have as little risk as possible. Low rates make money cheap for large institutions whose debt has low risk. Because investments are really a market in risk, the ‘interest rate’ is a lower bound for promised investment returns (denominated in the sovereign currency). Companies who cannot return the risk free rate shrink and die, so they can be replaced by stronger companies.

- A carry trade is a popular way to monetize the difference between interest rates in different economies. The trade consists of borrowing at a low rate in a low rate economy, and investing at a higher rate in a high rate economy. This results in a flow of capital into the higher-rate economy. The US during it’s good times benefited greatly from the inflows of carry trade capital brought in by the great Paul Volcker’s high-rate policies.

- ‘Money’ has so many purposes it’s definition is a significant philosophical problem (see: Geoffrey Ingham’s The Nature of Money). However for the purposes of this tract I’d like to consider two sorts of money separately: investment capital belonging to people whose wealth far exceeds material needs (which usually is intelligently invested at above the interest rate), and transactional capital held by normal workers (in bank accounts with little-or-no interest). I will take as granted that virtually all crypto is investment capital, since as a transaction medium, it sucks.

Inflows into Crypto are a Carry-Trade and will grow dramatically if nothing changes.

Inflation floats around the interest rate, but has a degree of flexibility. For average people who spend their money, it’s usually more important to think about the ‘real-rate’ which is the interest rate minus inflation. As the average American could tell you, real rates are negative right now. Money held in a bank account is really shrinking in buying power over time.

Meanwhile crypto has gone nowhere but up due to a variety of tailwinds (the rise of retail investing etc.). It certainly isn’t because it’s a better way to send money (ETH transactions cost 10$ or so right now as opposed to venmo’s 0$). I would argue that by far the strongest tailwind for crypto, is the fact that real money faces much more severe regulatory burdens. You can presently spend money on GPU’s, mine electricity into tokens in an anonymous wallet, and after 170 days or so have your money fully out of US regulatory sight all the while being invested in assets that have realized Sharpes far in excess of 2. If you mine into an anonymous wallet you can take that money anywhere, make gains on it etc. without incurring any tax or oversight (despite gruff messages and fist shaking from the US Government or EU). This is the main reason for the high premiums that mining supplies and mining services command (usually in excess of 30$ of the face value of coins mined). It’s a pretty standard money laundering overhead. Even physical gold faces more severe regulatory hurdles.

Because the US government is choosing to tax their legal money at 2% (with low rates) + capital gains etc., capital will continue to carry trade from USD into crypto-currencies. At time of writing about a twelfth as much institutional capital is invested in crypto as gold. By the end of 2022, I could easily see that being 50%. At that point any actions to try to restore the meaning of the dollar and slow flows into crypto would not be possible without quite severe political consequences. The US would basically be running two monetary systems, an unregulated one for speculators, and an onerous one for the poor who cannot engage in speculation.

Where is this going?

Basically there’s only a few possible scenarios:

- (best outcome) US regulators try to make traditional finance competitive. They raise rates and kill off the ludicrous retail boom in investing in zombie companies and large random prime numbers. They largely let crypto alone, besides stopping its use in dangerous crimes and tax evasion. They would also do well to waste less tax money. They allow ordinary people to participate in the same economy as banks, and remove barriers which bar ordinary people from investing in things like private equity.

- (most likely outcome) US regulators say a lot of things that sound like they are serious about regulating crypto, but continue to completely fail to understand (or ignore) even the basics of how crypto works. The crypto carry trade continues to the point where many high income people want/try to take all their income in the form of crypto. The USG has to react in a forceful, redistributive way to restore monetary control, or perhaps doesn’t and collapses.

- (boring outcome) US regulators find their missing competence bone. They require a full audit trail and only allow wallets which have never received anonymous monies to participate in the ordinary economy. They tax it like a speculative investment, and require full compliance on DeFi. Crypto slowly hemorrhages value under the regulatory compliance pressures.

I really do think the most likely outcome is not a great outcome.

US-Rates are too low, and that’s bad for normal people who live in the US.

Most people (correctly) associate rate increases with dips in the stock market, and therefore do not like them (even though they certainly should wish them to be raised now), let me explain why they are good.

Hedge fund customers get 3x leverage at almost no cost (rates are low) because their debts are considered near risk-free. They can buy high-grade corporate debt at an effective rate of ~21%, at basically no risk, because high grade debt is also considered low risk. There is no danger because the companies can cheaply refinance their endless balance sheets. A complex web of regulatory effects prevents most mom-and-dad’s from doing the same thing. The low productivity zombie corporations mom-and-dad work at shamble along, financed by record-high debt-to-value and debt-to-revenue. Mom and dad do not get new opportunities, because no matter how ossified and silly a corporation like IBM or Boeing is, the FED will not let them die. In the March 2020 emergency market actions, the FED bought 16$ of corporate debt from zombies like these for every dollar of relief stimulus given to individuals. It didn’t even buy them directly, it bought them in the form of Blackrock products (siphoning fee money directly to Blackrock from the US balance sheet). Naturally Blackrock was literally in the room telling policymakers to do so.

Besides the direct effects of low rates, there’s an indirect effect that low rates reverse the longstanding carry trade which brought foreign money in to buy US treasuries. This devalues the dollar as capital leaves the US money supply for higher rate greener pastures like crypto. This especially hurts mom-and-dad, who make little interest on their checking. Why do rate increases cause market dips? It’s pretty simple. If rates go up, our clients cannot access infinite cheap monies to invest, and will have to scale back their leveraged positions in equities. Markets are well aware of this, and respond in anticipation at the slightest whiff of rate increases. However these effects are transitory, and often quite healthy for the economy.

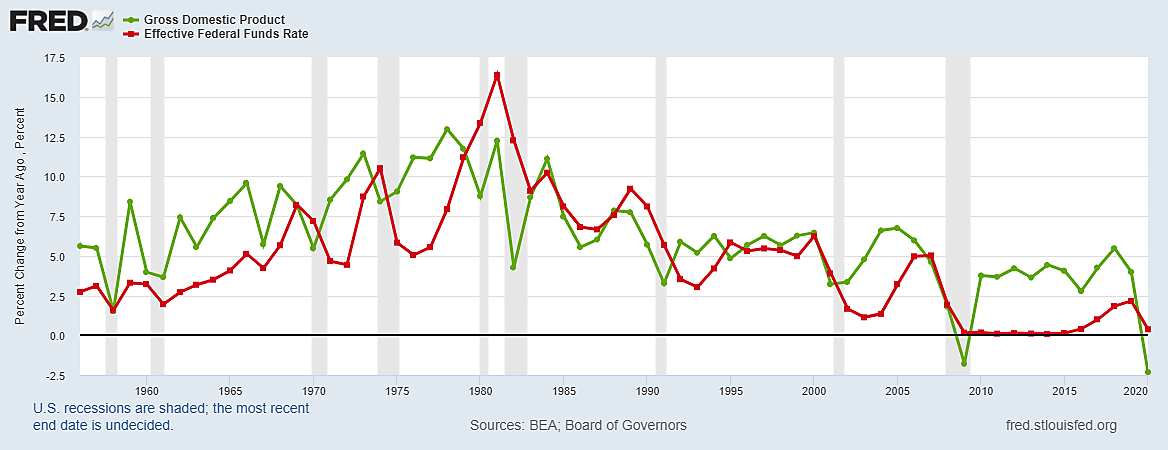

Its quite obvious from the plot below that contrary to the idea the higher rates cause meltdowns, the fed funds rate is really a delayed reaction to low GDP.

After an economic shock, the FED lowers rates to soften the blow after it’s been delivered. Even though high rates cause the economy to be more competitive and dynamic, few FED chairs ever choose to raise rates because no one wants to catch the hot potato of a market dip. This effect does much more for inequality than any political policy people actually vote about in my opinion.

After an economic shock, the FED lowers rates to soften the blow after it’s been delivered. Even though high rates cause the economy to be more competitive and dynamic, few FED chairs ever choose to raise rates because no one wants to catch the hot potato of a market dip. This effect does much more for inequality than any political policy people actually vote about in my opinion.

As for whatever might happen with crypto, I would argue that: